Understanding Delta and Its Role in Options Trading and Risk Management

- Jun 26, 2022

- 20 min read

Updated: Dec 17, 2025

In the derivatives market, understanding how option prices respond to changes in underlying market conditions represents one of the most crucial skills for both traders and risk managers. Among all the measures used to quantify this sensitivity, Delta stands as the most direct and widely used. Delta bridges the gap between the seemingly abstract world of option pricing and the concrete reality of profit and loss, providing traders with a quantifiable measure of directional risk and price sensitivity.

Delta represents far more than a simple mathematical derivative; it is the primary tool through which market participants understand, measure, and manage their exposure to price movements in the underlying asset. When a trader holds an option position, Delta answers the immediate and practical question: "How much will the position's value change if the stock moves up or down by one dollar?" This seemingly simple question underlies countless trading decisions, risk management strategies, and hedging operations executed daily in financial markets worldwide.

The importance of Delta extends across multiple dimensions of derivatives markets:

For traders, Delta provides essential information for position sizing, profit forecasting, and strategy selection. A trader contemplating buying call options needs to understand that different strikes offer varying Delta exposures, fundamentally affecting both the risk profile and profit potential of the position.

For risk managers, Delta represents the primary metric for measuring and controlling directional exposure across portfolios containing hundreds or thousands of option contracts. For market makers, Delta drives hedging decisions that allow them to provide liquidity while managing their own risk exposure.

Understanding Delta also opens the door to more sophisticated concepts in option pricing and risk management. Delta serves as the foundation for understanding the complete suite of option Greeks, such as Gamma, Theta, Vega, and Rho, each of which measures sensitivity to different market factors. Moreover, Delta is directly connected to fundamental concepts in option pricing theory, particularly the Black-Scholes-Merton model, where Delta emerges not just as a sensitivity measure but as a probability estimate related to the option's likelihood of expiring in-the-money (ITM).

We'll explore Delta from multiple perspectives, its mathematical definition, its practical calculation, its interpretation as both a sensitivity measure and a probability, its behavior across different market conditions, and its critical applications in trading and risk management. By understanding these concepts, you'll develop the foundational understanding necessary for sophisticated options trading and derivatives risk management.

Understanding Delta

Multiple Perspectives – Derivative Trader and Risk Manager – on a Single Concept

Definition 1: Delta as Rate of Change

The most fundamental definition of Delta describes it as the rate of change in an option's price with respect to changes in the underlying asset's price.

As per the definition,

Option Delta = Δ Option Price / Δ Underlying Price

Mathematically, this is expressed as a partial derivative:

Δ = ∂C/∂S (for call options) Δ = ∂P/∂S (for put options)

Where:

Δ represents Delta

C represents the call option price

P represents the put option price

S represents the underlying asset price

∂ denotes a partial derivative, indicating we're examining the change while holding all other factors constant

This definition characterizes Delta as a sensitivity measure; it quantifies how sensitive the option price is to movements in the underlying asset. The partial derivative notation emphasizes a crucial aspect of Delta: it measures the relationship between option price and underlying price while holding constant all other factors that affect option value, including time to expiration, volatility, interest rates, and dividends.

The concept of a partial derivative is essential here because option prices depend on multiple variables simultaneously. The underlying price is just one of several factors affecting option value. When we calculate or discuss Delta, we are isolating the effect of underlying price changes from the effects of time decay, volatility shifts, or other market changes. This isolation allows us to understand and quantify the specific impact of directional movements in the underlying asset.

In practical terms, this rate-of-change interpretation means that Delta captures the slope of the option price curve at any given point. If you were to graph the option price against the underlying price, Delta represents the slope of that graph at the current underlying price level. For call options, this slope is always positive, as the underlying rises, call values increase. For put options, the slope is negative, as the underlying rises, put values decrease.

Definition 2: Delta as Expected Price Change per Dollar Move

A more intuitive and practically oriented definition states that Delta represents the amount by which an option's price is expected to change for each one-dollar change in the underlying asset's price, with all other factors held constant.

Expected Change in Option Price = Δ x Change in Underlying Price

This definition translates the abstract concept of a derivative into concrete dollars and cents. If a call option has a Delta of 0.60, we expect the option's price to increase by approximately $0.60 for every $1 increase in the underlying stock price (and decrease by $0.60 for every $1 decrease).

The word "approximately" is crucial here. Delta provides a linear approximation of what is actually a curved relationship between option price and underlying price. This approximation works well for small moves in the underlying but becomes less accurate for larger moves, a limitation we'll explore when discussing Gamma.

Example:

The following 1-Day price movements:

Strike Price is $1490.00, Underlying Price changes from $1488.05 to $1498.05, Call Option Premium changes from $8.72 to $14.34, and Put Option Premium changes from $10.18 to $5.80

Therefore, using the sensitivity approach,

Call Option Delta = ∂C/∂S = (Ct - Ct-1) / (St - St-1) = (14.34 - 8.72) / (1498.05 - 1488.05) = 0.5620 represents that the price of a call option is expected to change by $0.5620 for every $1 change in the price of the underlying asset, same direction.

Put Option Delta = ∂P/∂S= (Pt - Pt-1) / (St - St-1) = (5.80 - 10.18) / (1498.05 - 1488.05) = -0.4380 represents that the price of a put option is expected to change by -$0.4380 for every $1 change in the price of the underlying asset, opposite direction.

Scenario 1: If the underlying stock price rises from $1488.05 to $1503.05:

Expected Price Change (for call option) = Δ x Change in Underlying Price = 0.5620 x 15 = $8.43

Call Option Price = $8.72 + $8.43 = $17.15

Expected Price Change (for put option) = Δ x Change in Underlying Price = -0.4380 x 15 = -$6.57

Put Option Price = $10.18 + -$6.57 = $3.61

Scenario 2: If the underlying stock price falls from $1488.05 to $1473.05:

Expected Price Change (for call option) = Δ x Change in Underlying Price = 0.5620 x -15 = -$8.43

Call Option Price = $8.72 + -$8.43 = $0.29

Expected Price Change (for put option) = Δ x Change in Underlying Price = -0.4380 x -15 = +$6.57

Put Option Price = $10.18 + $6.57 = $16.75

These approximation works best for the $1 move and become less precise for the larger $15 move due to the curvature in the option price/underlying price relationship.

Definition 3: Delta as Probability (Black-Scholes Model)

The Black-Scholes-Merton option pricing model provides a third, profound interpretation of Delta: for European options on non-dividend-paying stocks, Delta represents the probability that the option will expire ITM. As per the pricing function provided by the Black-Scholes-Merton (BSM) model,

In the Black-Scholes framework, the call option Delta equals N(d₁), where N represents the cumulative standard normal distribution function and d₁ is a specific value calculated from the option's parameters. Here, N(d1) is the probability that helps in determining the expected payoff in case the option is exercised (or expires in the money). As per explanation 3, N(d1) is called the option's delta.

The formula to arrive at this is provided by Black and Scholes in their pricing model.

In fact, this N(d₁) term has a dual interpretation- it is simultaneously the sensitivity of the option price to underlying price changes and the risk-neutral probability that the option will finish ITM at expiration.

For Call Options: Δcall = N(d₁)

For Put Options: Δput = N(d₁) - 1 = -N(-d₁)

This probabilistic interpretation provides powerful intuition for understanding Delta values:

At-the-Money (ATM) options have Delta near 0.50 for calls (-0.50 for puts), reflecting the roughly 50-50 probability that the option will expire in-the-money versus out-of-the-money.

In-the-Money (ITM) or Deep ITM options have Delta near 1.00 for calls (-1.00 for puts), reflecting the high probability (approaching certainty) that these options will expire in-the-money.

Out-of-the-Money (OTM) or Deep OTM options have a Delta near 0.00 for calls and puts, reflecting the low probability that these options will expire in-the-money.

The call option's Delta of 0.5620 suggests this is approximately ATM with roughly 56% probability of expiring ITM. This probabilistic interpretation helps traders understand why Delta changes as markets move. When a stock rallies, call options become more likely to expire ITM, so their Delta increases. On the other hand, put options become less likely to expire ITM, so their Delta (in absolute value) decreases.

The probability interpretation strictly applies to the risk-neutral probability measure used in option pricing theory, not necessarily to actual (physical) probabilities of market outcomes. Nevertheless, it provides valuable intuition for understanding Delta behavior.

Mathematically,

If the price of an underlying asset increases, the absolute value of the option delta of both call and put options increases too. However, the price of the Call Option increases, and that of the Put Option decreases.

If the price of an underlying asset decreases, the absolute value of the delta of both the call option and the put option decreases too. However, the price of the call option decreases, and that of the put option increases.

And because of this relationship, the delta of a call option always remains positive (it will range between 0 and 1, representing a positive relationship with the underlying), and the delta of a put option always remains negative (ranging between -1 to 0, representing a negative relationship with the underlying).

This ranging variable (Delta) may change depending upon the moneyness of an Option as far as we look into the direction of the underlying asset. However, it may also change due to the change in the volatility and time decay.

The Relationship Between Call and Put Delta

One of the most important mathematical relationships in options theory connects call Delta and put Delta for options with the same strike price and expiration:

Put Delta = Call Delta - 1, or Δput = Δcall - 1

For non-dividend-paying stocks, this can also be expressed as:

Δcall + |Δput| = 1

(the sum of the absolute values of call delta and put delta equals 1)

Or equivalently: Δcall - Δput = 1

This relationship emerges from put-call parity, one of the fundamental no-arbitrage conditions in options pricing. Put-call parity states that a portfolio containing a long call and a short put (with the same strike and expiration) is equivalent to a forward contract on the underlying asset.

For example,

If the delta of a call option is 0.5620, the delta of a put option is 0.5620 - 1 = -0.4380

It means that if the price of the underlying asset increases by $1, the price of a call option is expected to increase by $0.5620, and that of a put option to decrease by $0.4380.

In absolute terms: |0.5620| + |-0.4380| = 1

To understand why this relationship holds, consider what happens when the underlying asset moves by $1:

A call option with Delta 0.5620 gains $0.5620

A put option with the same strike loses -$0.4380

Together, the combination gains $0.5620 + -$0.4380 = $0.124

But wait, shouldn't a long call plus a short put behave like owning the underlying, which would gain the full $1? The apparent discrepancy disappears when we remember that options have strike prices. The $0.124 net gain represents the difference between the $1 move in the underlying and the fixed strike price relationship. When properly accounting for the present value of the strike price, the put-call parity holds exactly.

A more direct intuition comes from recognizing that a long stock position can be replicated by:

Long call + Short put (at the same strike)

Plus an appropriate bond position

Since a long stock position has Delta = 1 (it moves dollar-for-dollar with the underlying), and since long call + short put replicates this exposure, we must have:

Δcall - Δput = 1

Therefore: Δput = Δcall - 1

The Dividend Adjustment

The relationship Δput = Δcall - 1 holds exactly for non-dividend-paying stocks. For dividend-paying stocks, the relationship becomes:

Δput = Δcall - exp(-qT)

Where:

q is the continuous dividend yield

T is time to expiration

exp(-qT) is the present value of receiving one unit of the underlying at expiration

The adjustment reflects that owning a stock that pays dividends provides value beyond the capital appreciation captured by Delta. The dividend yield reduces the effective forward price of the stock, which affects the put-call parity relationship.

We can verify the put-call Delta relationship using our earlier example:

Call Delta = 0.5620, Put Delta = -0.4380

Check: 0.5620 + |-0.4380| = 0.5620 + 0.4380 = 1

Or equivalently: -0.4380 = 0.5620 - 1

This verification confirms that our empirically calculated Deltas satisfy the theoretical relationship, providing confidence in both the calculations and the underlying theory.

Delta in Practice – Option Trading and Risk Management

Using Delta to Forecast Position Value Changes: One of the most immediate practical applications of Delta involves forecasting how option position values will change in response to underlying price movements. This capability is essential for position sizing, profit targeting, and risk assessment.

Single Option Position: A trader holding 10 call option contracts (each representing 100 shares) with Delta = 0.65: Position Delta = Number of Contracts x Contract Multiplier (Lot Size) x Delta per Share = 10 x 100 x 0.65 = 650

This position Delta of 650 means the position behaves like owning 650 shares of the underlying stock. If the stock moves $1: Expected Position Value Change = Position Delta x Spot Shock = 650 x $1 = $650

If the trader expects the stock to rise $5 based on earnings expectations, the Expected Position Gain = 650 x $5 = $3,250. This forecast helps the trader assess whether the potential reward justifies the premium paid and the risk taken.

Portfolio-Level Delta: For portfolios containing multiple option positions, total Delta is the sum of individual position Deltas:

Long 5 contracts of $100 strike calls, Delta = 0.60: Position Delta = +300

Short 3 contracts of $105 strike calls, Delta = 0.40: Position Delta = -120

Long 2 contracts of $95 strike puts, Delta = -0.55: Position Delta = -110

Total Portfolio Delta = 300 - 120 - 110 = +70

This portfolio has a net Delta of +70, meaning it will gain approximately $70 for each $1 increase in the underlying (and lose $70 for each $1 decrease). The relatively small net Delta despite multiple positions indicates a relatively hedged or neutral stance.

Delta-Neutral Hedging: Delta-neutral hedging represents one of the most important applications of Delta in professional options trading and market making. The goal is to construct a portfolio whose value is insensitive to small moves in the underlying asset, isolating other sources of profit or risk.

A delta-neutral position has total Delta = 0, meaning its value doesn't change (theoretically) with small moves in the underlying. This is achieved by combining options with offsetting Deltas or by combining options with positions in the underlying stock.

Example: A trader owns 10 call option contracts (1,000 options) with Delta = 0.60: Position Delta = 1,000 × 0.60 = +600

To delta-hedge this position using the underlying stock: Required stock position = -Position Delta = -600 shares (short)

By shorting 600 shares of stock, the trader creates a delta-neutral portfolio:

Options Delta: +600

Stock Delta: -600 (since stock has Delta = 1.00)

Net Delta: 0

Now, if the stock moves $1 in either direction:

Options Gain/Loss: $600

Stock Position Loses/Gains: $600

Net Change: $0 (approximately)

But, Delta is not constant; it changes as the underlying moves, time passes, and volatility shifts. This means that a delta-neutral position doesn't remain neutral without active management. The need to continuously adjust hedge ratios is called "dynamic hedging."

Initial Position:

Long 1,000 Call Options, Delta = 0.60

Short 600 Shares (as hedge)

Net Delta = 0 (neutral)

Stock Increases by $10:

Call Delta Increases to 0.75 (due to Gamma)

New Option Position Delta = 1,000 × 0.75 = +750

Stock Delta (as hedge) = -600 (unchanged)

Net Delta = +150 (no longer neutral)

To restore neutrality, the trader must short an additional 150 shares, bringing the total stock short position to 750 shares. The frequency of rehedging depends on several factors:

Gamma: Higher Gamma means Delta changes faster, requiring more frequent rehedging.

Transaction costs: Each rehedge incurs commissions and bid-ask spreads.

Market volatility: More volatile markets require more frequent rehedging.

Risk tolerance: Some tolerance for being off-neutral reduces hedging costs.

Professional market makers might rehedge continuously throughout the day, while other traders might rehedge daily or weekly, depending on their strategy and cost considerations.

The important point to note here is that the option sensitivities are in terms of a unit change in a single risk factor, while keeping other risk factors constant, unlike elasticity (stated in terms of percentage change in one factor), scenarios, or simulation (simultaneous change in multiple risk factors).

Why Would a Trader Want to Delta-Neutralize a Position?

Market makers use delta-neutral hedging to provide liquidity without taking directional risk. They profit from the bid-ask spread and volatility, not from directional bets.

Volatility traders create delta-neutral positions to isolate their exposure to implied volatility changes rather than directional moves.

Risk management uses delta-neutral hedging to reduce exposure during uncertain periods while maintaining positions for other reasons (tax timing, conviction in long-term thesis, etc.).

Practical Implementation: Delta Using Black-Scholes and Insights

(options delta series across the spot ladder at a particular strike price)

Using the Black-Scholes formula,

d1 = ln(1488.05 / 1490.00) + (0.06 + 1/2 * 0.2145^2) * 0.0055 / 0.2145 * 0.0055 = -0.053

N(d1) = N(-0.053) ≈ 0.04785

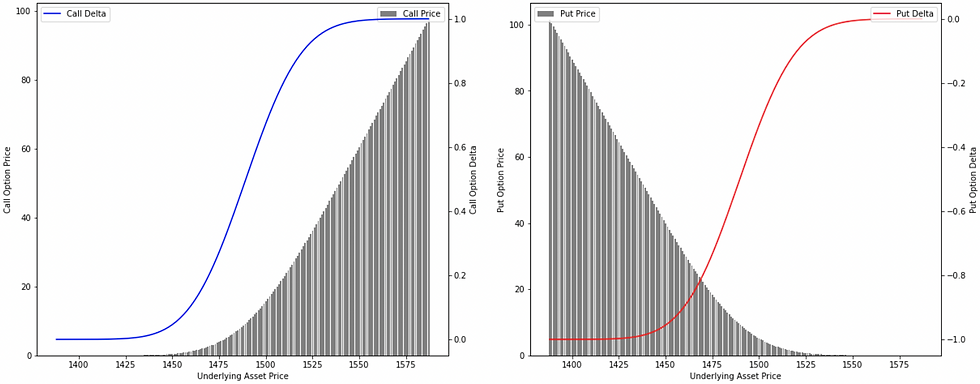

Let's examine how Delta changes across different underlying prices for options with a fixed strike of $1,490.00, using the Black-Scholes model:

Delta is not constant; it changes as the underlying asset price changes, as time passes, and as volatility shifts. Understanding how Delta responds to these factors is crucial for effective options trading and risk management.

How Delta Changes with Underlying Price: The relationship between Delta and the underlying price depends on the option's moneyness; whether it is in-the-money (ITM), at-the-money (ATM), or out-of-the-money (OTM):

For Call Options:

Deep OTM: Delta approaches 0. When the stock price is far below the strike price, the call has a very low probability of expiring ITM. The option price is minimally sensitive to underlying price changes.

Example: As the price of the underlying asset decreases (from ATM to OTM to deep OTM, i.e., from $1488.05 to $1478.05 to $1468.05), the delta of the call option also decreases (from 0.4785 to 0.3162 to 0.1825). As the option gets further OTM, the probability that the option will land ITM decreases, and therefore, the call option's delta also decreases. This makes the deep OTM call options less attractive as the probability of their getting exercised is low, and therefore, the delta of a deep OTM call option is also low.

ATM: Delta ≈ 0.50. When the stock price equals the strike price, there's roughly a 50-50 probability of expiring ITM. The option shows moderate sensitivity to underlying price changes. This 0.50 Delta is a key reference point for options traders. The probability of the option landing ITM is 50%, and therefore, the delta of an ATM call option remains close to 0.5, and that of an ATM put option is -0.5.

Deep ITM: Delta approaches 1.00. When the stock price is far above the strike price, the call has a very high probability of expiring ITM. The option price moves almost dollar-for-dollar with the underlying.

Example: As the price of the underlying asset increases (from ATM to ITM to deep ITM, i.e., from $1488.05 to $1498.05 to $1508.05), the delta of the call option also increases (from 0.4785 to 0.6435 to 0.7843). As the option gets further ITM, the probability that the option will land ITM increases, and therefore, the call option's delta also increases. This makes the deep ITM call options more attractive as the probability of their getting exercised is high, and therefore, the delta of a deep ITM call option is also high.

For Put Options:

Deep OTM: Delta approaches 0. When the stock price is far above the strike price, the put has a very low probability of expiring ITM. The option price is minimally sensitive to underlying price changes.

Example: As the price of the underlying asset increases (from ATM to OTM to deep OTM, i.e., from $1488.05 to $1498.05 to $1508.05), the absolute value of delta of the put option decreases (from -0.5278 to -0.3624 to -0.2204). As the option gets further OTM, the probability that the option will land ITM decreases, and therefore, the put option's delta also decreases. This makes the deep OTM put options less attractive as the probability of them getting exercised is low, and therefore, the delta of a deep OTM put option is also low.

ATM: Delta ≈ 0.50. When the stock price equals the strike price, there's roughly a 50-50 probability of expiring ITM. The option shows moderate sensitivity to underlying price changes. This 0.50 Delta is a key reference point for options traders. The probability of the option landing ITM is 50%, and therefore, the delta of an ATM call option remains close to 0.5, and that of an ATM put option is -0.5.

Deep ITM: Delta approaches 1.00. When the stock price is far above the strike price, the call has a very high probability of expiring ITM. The option price moves almost dollar-for-dollar with the underlying.

Example: As the price of the underlying asset decreases (from ATM to ITM to deep ITM, i.e., from $1488.05 to $1478.05 to $1468.05), the absolute value of delta of the put option increases (from -0.5278 to -0.6895 to -0.8217). As the option gets further ITM, the probability that the option will land ITM increases, and therefore, the put option's delta also increases. This makes the deep ITM put options more attractive as the probability of them getting exercised is high, and therefore, the delta of a deep ITM call option is also high.

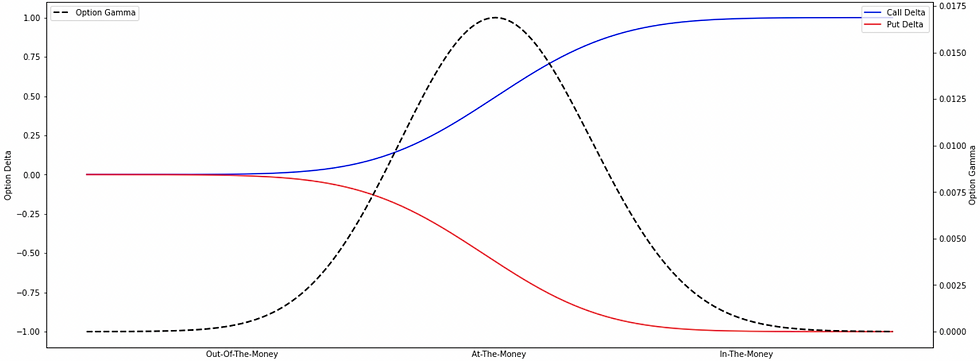

This 50% Delta point serves as a crucial reference for traders. ATM options are often quoted as "50-Delta options", and many options strategies are built around this reference point. The 50-Delta level represents maximum uncertainty about the option's terminal value, which has important implications for both pricing and risk management.

As the underlying price increases:

Call Delta increases monotonically from near 0 to near 1.00

Put Delta increases (becomes less negative) from near -1.00 to near 0

This monotonic relationship reflects the increasing/decreasing probability of expiring ITM as the underlying moves relative to the strike. Each incremental increase in the underlying price makes calls more likely to expire ITM and puts less likely to expire ITM.

The Delta curve is not linear; it's S-shaped (sigmoidal). This curvature is most pronounced near the at-the-money point and flattens out for deep ITM and OTM options:

Near ATM (underlying $1,478-$1,508): Delta changes rapidly with the underlying price. Small moves in the underlying create significant Delta changes. Call Delta ranges from 0.3162 to 0.7843 across a $30 range. This steep slope region represents maximum sensitivity to underlying price changes

Deep ITM/OTM (extremes of the range): Delta changes slowly with the underlying price. Large moves in the underlying create modest Delta changes. Deep OTM call (underlying $1,468): Delta = 0.1825. Deep ITM call (underlying $1,518): Delta = 0.8824. The curve flattens as Delta approaches its limits (0 or 1)

This S-shaped curve has profound implications.

The steepness near ATM means that ATM options have high Gamma (the rate of change of Delta, second-order derivative), making them particularly dynamic and requiring active hedging. The flatness at extremes means deep ITM/OTM options have low Gamma, making their Delta relatively stable.

This is because the near ATM options are more sensitive to changes in the price of the underlying asset, as these options have a nearly 50% probability of being exercised and a nearly 50% probability of being lapsed. This creates uncertainty in the minds of traders, leading to a higher number of buy-sell positions, which in turn results in higher variability in the option's delta, as shown above.

The table above also reveals the relationship between Delta and option intrinsic/extrinsic value:

Deep ITM (high Delta) options consist primarily of intrinsic value with minimal time value. The call at $1,518.05 is worth $29.89, of which $28.05 is intrinsic value ($1,518.05 - $1,490.00) and only $1.84 is time value.

ATM (Delta ≈ 0.50) options consist entirely of time value with no intrinsic value. The call at $1,490.00 is worth $6.12, all of which represents time value.

Deep OTM (low Delta) options have only time value, but very little of it. The call at $1,468.05 is worth only $2.30, entirely the time value, reflecting the low probability of expiring ITM.

This relationship between Delta and option composition helps traders understand what they're buying when they purchase options at different strikes. High-Delta options are primarily bets on directional movement (since they're mostly intrinsic value), while low-Delta options are primarily bets on volatility and time (since they're entirely time value).

Delta and Time Decay: Delta and Theta (time decay sensitivity) interact in important ways:

ATM: ATM options have maximum time value and thus the highest Theta (fastest time decay). They also have Delta near 0.50. As time passes, Call Delta may decrease slightly toward 0.50 (if slightly ITM) or increase toward 0.50 (if slightly OTM). Time decay erodes option value, but Delta remains relatively stable near 0.50. The high Theta represents the price of high Gamma exposure.

Deep ITM: Deep ITM options have high Delta but low time value and thus low Theta. Time decay has minimal impact on these options, which behave mostly like stock positions.

Deep OTM: OTM options have low Delta and moderate Theta. As expiration approaches, Delta drifts toward zero (the probability of expiring ITM decreases). Time decay accelerates. The option becomes increasingly worthless.

Delta and Implied Volatility: Changes in implied volatility affect Delta, though the relationship is subtle:

ATM: Volatility changes have a minimal direct effect on ATM Delta, which remains near 0.50 regardless of volatility level. However, volatility affects the option's price and Gamma significantly.

Deep OTM: Increasing volatility increases OTM option Delta: Higher volatility increases the probability of finishing ITM. Delta increases to reflect this higher probability. Example: OTM call with Delta 0.20 might move to 0.25 if volatility spikes.

Deep ITM: Increasing volatility slightly decreases ITM option Delta: Higher volatility introduces more uncertainty about finishing ITM. Delta decreases slightly from very high levels. Example: ITM call with Delta 0.85 might move to 0.82 if volatility spikes.

Volatility spikes tend to compress the Delta distribution (OTM Deltas increase, ITM Deltas decrease slightly), make the Delta curve less steep near ATM (lower Gamma), and create more balanced probability distributions across strikes.

In reality, options at different strikes don't follow a single implied volatility—the volatility smile or skew means different strikes have different implied volatilities. This affects how Delta behaves across strikes.

Common Misconceptions and Pitfalls

Delta is Constant: Perhaps the most dangerous misconception is treating Delta as a constant. New options traders sometimes calculate Delta at trade initiation and assume it remains fixed throughout the trade's life. In reality, Delta changes continuously due to:

Underlying Price Movements (via Gamma)

Time Decay (approaching expiration)

Volatility Changes (via Vega)

Interest Rate Changes (via Rho)

A position that starts with Delta 0.50 might end with Delta 0.80 (if underlying rallies) or Delta 0.20 (if underlying declines), fundamentally changing the position's risk profile. Best Practice: Monitor Delta continuously, especially for positions with high Gamma or approaching expiration. Update forecasts and hedge ratios regularly based on current Delta, not initial Delta.

Delta Perfectly Predicts Price Changes: Delta provides a linear approximation of option price changes, but the actual relationship between option price and underlying price is curved (convex). This leads to prediction errors, especially for large underlying moves.

Example: Option with Delta 0.60 and Gamma 0.04, initial price $5.00:

Small move (stock +$1): Delta Prediction: +$0.60 and Actual Change (including Gamma): ≈+$0.62

Error: Small (≈3%)

Large move (stock +$10): Delta Prediction: +$6.00 (10 x 0.60) and Actual Change (with Gamma effects): ≈+$7.50

Error: Large (≈25%)

The Delta-only approximation increasingly understates gains (for calls) or losses (for puts) as moves become larger, because Gamma creates convexity that accelerates changes. Best Practice: Use Delta for forecasting small moves, but incorporate Gamma for larger anticipated moves. Or use full option pricing models to revalue positions for significant underlying changes.

Higher Delta is Always Better: Beginners sometimes assume higher Delta call options are "better" because they're more sensitive to underlying moves. This ignores several factors:

Capital Efficiency: Low-Delta OTM options cost less, providing more leverage per dollar invested (though with a higher risk of total loss).

Probability: High-Delta options have a higher probability of profit but smaller percentage returns. Low-Delta options offer lottery-ticket potential with lower probability.

Gamma and Time Decay: High-Delta ITM options have low Gamma (stable but boring) and low Theta (minimal decay). Low-Delta OTM options have higher Gamma (more dynamic) but higher Theta (faster decay).

Best Practice: Choose Delta based on market view, risk tolerance, time horizon, and capital constraints. Different Deltas suit different situations; there's no universally "best" Delta.

Delta-Neutral Means Risk-Free: Creating a delta-neutral position eliminates directional risk but doesn't eliminate all risk:

Gamma Risk: The position's Delta will change as the underlying moves, creating exposure unless continuously rehedged.

Vega Risk: Volatility changes affect the position's value even with zero Delta.

Theta Risk: Time decay continues regardless of Delta.

Transaction Costs: Continuous rehedging to maintain neutrality incurs costs that can erode profits.

Gap Risk: If the underlying gaps (open significantly away from the previous close), the hedging relationship breaks down.

Best Practice: Understand that delta-neutral means neutral to small moves only. Other Greeks and practical considerations still create substantial risk.

Put-Call Parity Always Gives Equal Absolute Deltas: While the relationship Δcall - Δput = 1 (or exp(-qT) for dividends) always holds, this doesn't mean |Δcall| = |Δput|. This equality occurs only ATM:

ATM: Δcall ≈ 0.50, Δput ≈ -0.50 (equal absolute values).

ITM: Δcall = 0.80, Δput = 0.80 - 1 = -0.20 (very different absolute values).

OTM: Δcall = 0.25, Δput = 0.25 - 1 = -0.75 (very different absolute values).

Best Practice: Don't assume symmetry between call and put Deltas except at ATM. For hedging or strategy construction, always calculate the specific Delta rather than assuming equality.

Delta represents far more than a simple sensitivity measure; it forms the conceptual foundation upon which all option trading and risk management is built. Through its multiple interpretations as a rate of change, a price sensitivity, and a probability measure, Delta provides the essential link between abstract option pricing theory and practical trading applications.

For traders, Delta translates complex option positions into understandable terms- "this position behaves like owning 500 shares" or "this portfolio will gain $2,000 for each point the market rises". This translation enables rational position sizing, realistic profit forecasting, and effective strategy selection. By understanding how Delta varies with moneyness, time, and volatility, traders can anticipate how their positions will evolve and adapt their strategies accordingly.

For risk managers, Delta provides the primary metric for measuring and controlling directional exposure. Whether managing a single portfolio or aggregating risk across an entire institution, Delta allows risk exposures to be quantified, monitored, and hedged on a common scale. The concept of delta-neutral hedging, while practically complex, provides a powerful framework for isolating and managing different sources of risk.

For students of finance, mastering Delta opens the door to a deeper understanding of option pricing theory. The relationship between Delta and the Black-Scholes model, the connection to risk-neutral probabilities, and the interplay with other Greeks all become accessible once Delta is thoroughly understood. These connections reveal options not as isolated bets but as sophisticated instruments that can be precisely calibrated to specific risk-return profiles.

Comments