Financial Derivatives And Risk Management: A Theoretical Interview Guide on Financial Derivatives (1.0)

- Aug 21, 2024

- 18 min read

Updated: Sep 14, 2024

Congratulations! You've landed an interview I understand, and now it's time to prepare for it!

One of the most important guides at your disposal is this interview guide. think of it as your roadmap to success, guiding you through the twists and turns of the interview process. Here's how to decode and utilize this essential document effectively.

Start by carefully reading through this interview guide from start to end. Pay attention to any instructions, formatting, or specific questions provided.

Spend time on each topic, take notes, strive for understanding, and, most importantly, attempt to model these complex problems using either Excel or Python.

While this interview guide provides a detailed framework, be prepared to adapt and think on your feet. Interviewers may ask unexpected or follow-up questions to test deeper into certain areas.

After the interview, reflect on your performance and seek feedback from trusted sources, such as mentors, career advisors, or interview coaches. Again, take notes of areas of improvement and incorporate them into your preparation for future interviews.

A Theoretical Interview Guide on Financial Derivatives – Options, Futures, Forwards, And Swaps

What are Derivatives?

Derivatives are financial contracts whose value is derived from the price of an underlying asset, index, or rate. The underlying asset can be anything (from equity stocks, interest-rate bonds, commodities, currencies, or market indices).

Derivatives are used for various purposes, such as hedging risk exposures, speculation, or arbitrage. It allows investors to control a large position in the underlying asset with a relatively small amount of capital. It enables market participants to transfer risk associated with the price movement of the underlying asset.

What are "options" in the derivatives market?

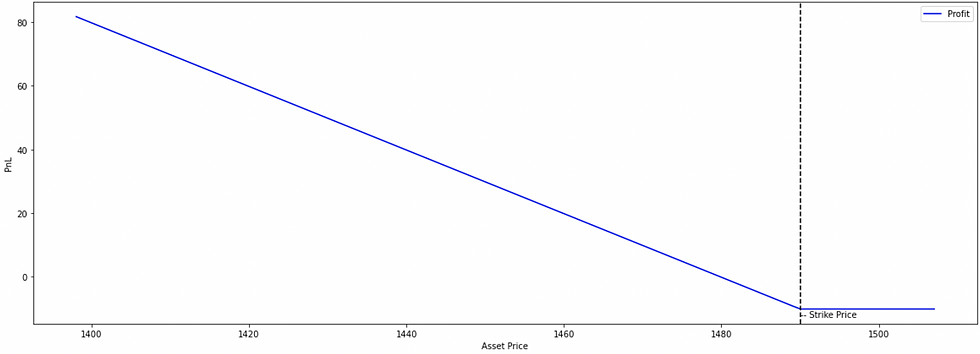

An option is a contract between the contracting parties to buy-sell an underlying asset at a pre-determined price (known as the strike price) for a pre-determined quantity (known as contracts having lot size) on a pre-determined later date (known as maturity/expiry date). A buyer of an option has a right to buy (in case of a call option) or sell (in case of a put option) but not an obligation to do so, and therefore, options are a non-linear product.

A call option is a financial contract that gives the buyer the right, but not the obligation, to purchase an underlying asset (such as a stock), at a specified price (known as strike price) to be transacted on a predetermined date (maturity date). And for the right, the buyer pays a premium.

Investors buy call options when they anticipate that the price of the underlying asset will rise above the strike price before the option expires. the seller (writer) of the call option is obligated to sell the asset if the buyer chooses to exercise the option. Call options are commonly used for speculation or hedging against potential price increases in the market.

A put option is a financial contract that gives the buyer the right, but not the obligation, to sell an underlying asset, such as a stock, at a specified price (known as strike price) to be transacted on a predetermined date (maturity date) in the future. And for the right, the buyer pays a premium.

Investors buy put options when they expect the price of the underlying asset to fall below the strike price before the option expires. the seller (writer) of the put option is obligated to buy the asset if the buyer decides to exercise the option. Put options are commonly used for speculation or hedging against potential declines in the market.

What is the difference between an option buyer and an option seller?

the key difference lies in their rights and obligations.

Option Buyer: the buyer of an option (whether it's a call or put option) has the right, but not the obligation, to either buy (in the case of a call option) or sell (in the case of a put option) the underlying asset at a predetermined price (strike price). the buyer pays a premium for this right, and their risk is limited to this premium paid.

Option Seller: the seller (writer) of an option, on the other hand, takes on an obligation. If the buyer exercises the option, the seller must fulfill the contract terms—either selling (for a call option) or buying (for a put option) the underlying asset. The seller receives the premium paid by the buyer as compensation but faces potentially unlimited risk if the market moves unfavorably.

What is the difference between the Strike Price and the Stock Price in an options contract?

the difference between the strike price and the stock price is as follows:

Strike Price: the strike price (or exercise price) is the price at which the holder of an option can buy (in the case of a call option) or sell (in the case of a put option) the underlying asset if they choose to exercise the option. It is a fixed price set at the time the option contract is created.

Stock Price: the stock price (or market price) is the current trading price of the underlying asset in the market. It fluctuates based on supply and demand dynamics, market sentiment, and other factors.

What is the moneyness of an option?

The moneyness of an option can be of three types:

In-the-money (ITM) options: A call option is considered to be ITM when its underlying asset price is trading above its strike price. A put option is considered to be ITM when its underlying asset price is trading below its strike price.

Out-of-the-money (OTM) options: A call option is considered to be OTM when its underlying asset price is trading below its strike price. A put option is considered to be OTM when its underlying asset price is trading above its strike price.

At-the-money (ATM) options: A call and a put option are considered to be ATMs when their underlying asset price is equal to their strike price.

What is the difference between Historical Volatility and Implied Volatility of an option?

the difference between historical volatility and implied volatility lies in what they measure and how they are calculated:

Historical Volatility: Historical volatility (also known as realized volatility) measures the actual price fluctuations of an asset over a specific past period. It reflects how much the asset's price has varied from its average over that time. It is typically calculated using the standard deviation of the asset's returns over a given time period, such as the past 250 trading days.

Implied Volatility: Implied volatility represents the market's expectation of how much the price of an asset will fluctuate in the future. It is derived from the current price of options on that asset. Implied volatility is calculated by inputting the current market price of an option into an options pricing model (such as Black-Scholes-Merton model) and solving for the volatility value that would make the model's price match the market price.

What is the difference between Volatility Skew and the Volatility Surface?

the difference between volatility skew and the volatility surface lies in the complexity and the dimensions they represent when visualizing implied volatility for options.

Volatility Skew: Volatility skew refers to the pattern of implied volatility across different strike prices for options with the same expiration date. It shows how implied volatility changes as the strike price moves away from the at-the-money (ATM) level. Volatility skew is typically a two-dimensional curve that plots implied volatility on the Y-axis and strike price on the X-axis for a single expiration date.

types of Skew: Positive Skew (Forward Skew): Implied volatility increases as the strike price increases. Negative Skew (Reverse Skew): Implied volatility decreases as the strike price increases.

If you look at the skew for options expiring in one month, you may notice that out-of-the-money puts have higher implied volatility than out-of-the-money calls, indicating a negative skew, which is common in equity markets due to demand for downside protection.

Volatility Surface: the volatility surface is a three-dimensional representation that shows implied volatility not just across different strike prices (like the skew) but also across different expiration dates. It provides a more comprehensive view of implied volatility for options on the same underlying asset. the volatility surface adds a third dimension—time to expiration—making it a three-dimensional plot with implied volatility on the x-axis, strike price on the y-axis, and expiration date on the z-axis.

Unlike the skew, which focuses on a single expiration date, the volatility surface allows you to see how implied volatility varies across both strike prices and expiration dates. It captures the full range of market expectations.

Traders and risk managers use the volatility surface to assess market conditions and price complex options strategies that involve multiple expiration dates and strike prices, such as calendar spreads or diagonal spreads.

»» Volatility Skew is a two-dimensional concept focused on how implied volatility changes with strike prices for a particular expiration date. Volatility Surface is a three-dimensional concept that incorporates both strike prices and expiration dates, providing a broader view of how implied volatility behaves across the entire options market for a specific underlying asset.

What is the difference between American, European, and Bermudan options?

Options come in different styles based on when the holder is allowed to exercise them. The most common styles are American, European, and Bermudan options. Here's an explanation of each:

American Options: American options allow the holder to exercise the option at any time up until the expiration date. This flexibility gives the holder the opportunity to take advantage of favorable market conditions at any point before the option expires. If you hold an American call option on a stock, and the stock price rises significantly before the expiration date, you can choose to exercise the option immediately to lock in your profit.

European Options: European options can only be exercised at expiration and not before. The holder has no flexibility to exercise early; they must wait until the expiration date to decide whether to exercise the option based on the final settlement price. If you hold a European call option on an index, you cannot exercise it before the expiration date, regardless of how favorable the price movement may be during the life of the option.

Bermudan Options: Bermudan options are a hybrid of American and European options. They can be exercised on specific dates during the life of the option, which are predetermined and often occur at regular intervals (for example, once a month or once a quarter). These options offer more flexibility than European options but less than American options. If you hold a Bermudan option, you may have the right to exercise it only on the first of every month up until expiration. If the underlying asset's price reaches a favorable level on one of those dates, you can exercise the option.

»» the key difference among these options lies in the flexibility of when the option can be exercised. American options can be exercised any time before expiration. European options can only be exercised at expiration. Bermudan options can be exercised on specific dates before expiration.

How can options derivatives be used in the financial market?

One common use of call options is to hedge against market increases. By purchasing put options, an investor can protect their portfolio against potential losses in the event that the underlying asset declines in value.

Call and put options can also be used to generate income through selling/writing options. When an investor sells a call or a put option, they collect a premium from the buyer in exchange for the obligation to potentially sell (in case of call option) or buy (in case of put option) the underlying asset at a later date.

Options can also be used to speculate on market movements. for example, an investor who believes that the price of an underlying asset will increase in the future may purchase call options as a way to profit from the potential price increase or an investor who believes that the price of an underlying asset will decline in the future may purchase put options as a way to profit from the potential price decline.

What are the differences between hedging, speculation, and arbitrage?

The differences between hedging, speculation, and arbitrage lie in their objectives and how they manage risk and potential returns:

Hedging: the primary goal of hedging is to reduce or eliminate risk associated with adverse price movements in an asset. Hedgers use derivative instruments, such as options or futures, to protect themselves from potential losses. A wheat farmer might use futures contracts to lock in a selling price for their crop, thereby hedging against the risk of falling wheat prices before harvest. Hedging is risk-averse; it sacrifices some potential profit in exchange for reducing exposure to negative price movements.

Speculation: It involves taking on risk with the expectation of earning a profit from future price movements in an asset. Speculators do not seek to protect against existing risks but instead aim to profit from market volatility. A trader might buy call options on a stock, expecting its price to rise in the near future, thus profiting from the increase. Speculation is risk-seeking; it involves taking on higher levels of risk in pursuit of potential gains.

Arbitrage: It aims to exploit price inefficiencies between markets to earn a risk-free profit. Arbitrageurs simultaneously buy and sell the same or equivalent assets in different markets to take advantage of price discrepancies. An arbitrageur might buy a stock on one exchange where it is undervalued and sell it on another exchange where it is overvalued, locking in a profit without taking on price risk. Arbitrage is considered risk-free or low-risk, as it involves taking advantage of market inefficiencies rather than betting on market direction.

»» Hedging is about reducing risk, often at the expense of some potential profit. Speculation is about taking on risk with the goal of earning profit from market movements. Arbitrage is about exploiting price differences in different markets to earn risk-free profit.

What’s the difference between hedging using forwards vs options?

The difference between hedging using forwards and options primarily revolves around the obligations, flexibility, and potential outcomes for the hedger:

Hedging with Forwards:

Obligation: When using a forward contract to hedge, both parties are obligated to fulfill the contract terms at the agreed-upon future date. This means the buyer must purchase, and the seller must deliver the underlying asset at the specified price.

Outcome: The outcome is certain; the hedger locks in a price, ensuring protection against unfavorable price movements but also forgoing any potential benefit from favorable movements. If the market moves in a favorable direction, the hedger still must transact at the forward price, potentially missing out on gains.

Cost: Typically, entering into a forward contract has no upfront cost, as it’s a bilateral agreement without premium payments.

for example, A company expecting to receive payment in foreign currency in six months may use a forward contract to lock in the exchange rate today, avoiding the risk of currency depreciation.

Hedging with Options:

Obligation: Options provide the right, but not the obligation, to buy (call option) or sell (put option) the underlying asset at a specified price within a certain timeframe. The hedger can choose whether or not to exercise the option based on market conditions.

Outcome: Options provide more flexibility. If the market moves favorably, the hedger can allow the option to expire and benefit from the market price. If the market moves unfavorably, the hedger can exercise the option to mitigate losses. This makes options a more flexible, albeit more expensive, hedging tool.

Cost: Options require the payment of a premium upfront. This cost is non-refundable and represents the price of the flexibility that options provide.

for example, An investor holding a stock may buy a put option to hedge against a potential decline in the stock’s value. If the stock price falls, the investor can exercise the option and sell the stock at the higher strike price.

What is a Swap Derivative?

A swap is a derivative contract in which two parties agree to exchange cash flows or other financial instruments over a specified period. The most common types of swaps involve exchanging cash flows based on different interest rates, currencies, or other financial metrics. Swaps are typically used for hedging risks or speculating on changes in market conditions.

On Agreement: Two parties agree on the terms of the swap, including the notional principal (the amount on which the exchanged payments are based), the duration of the swap, and the schedule of payments.

Intermediate Exchange: The parties exchange cash flows according to the agreed schedule. For example, in an interest rate swap, one party might pay a fixed rate while receiving a floating rate, with payments made semi-annually.

On Settlement: At the end of the swap’s term, any final payments are made, and the swap contract is settled.

for example,

Party A has a loan with a floating interest rate of LIBOR + 1% on a $10 million notional principal.

Party B has a fixed-rate loan at 5% on the same notional principal but prefers a floating rate.

they enter into an interest rate swap agreement where:

Party A agrees to pay Party B a fixed rate of 4% on the $10 million notional.

Party B agrees to pay Party A the floating rate of LIBOR + 1% on the $10 million notional.

Every quarter, Party A pays the fixed 4% to Party B, and Party B pays the floating LIBOR + 1% to Party A.

Instead of exchanging the total interest payments, they only exchange the net difference between the two amounts. this simplifies the transaction and reduces credit risk.

this type of swap allows Party A to convert their floating-rate loan into a fixed-rate loan at 4%, while Party B effectively converts their fixed-rate loan into a floating-rate loan at LIBOR + 1%.

Different Types of Swaps:

Interest Rate Swaps: An interest rate swap involves the exchange of interest rate payments between two parties. One party pays a fixed interest rate, while the other pays a floating (variable) interest rate, based on a reference rate like LIBOR. A company with a floating-rate loan might enter into a swap to exchange its floating-rate payments for fixed-rate payments, thereby locking in a stable interest expense.

Currency Swaps: In a currency swap, the parties exchange principal and interest payments in different currencies. This type of swap is used to hedge or speculate on currency fluctuations or to obtain financing in a foreign currency at a more favorable rate. A U.S. company needing euros might swap its dollar-denominated payments with a European company needing dollars, each benefiting from the other's currency access.

Commodity Swaps: Commodity swaps involve exchanging cash flows based on the price of a commodity, such as oil or gold. One party pays a fixed price, while the other pays a floating price based on the current market rate. An airline might use a commodity swap to lock in the price of jet fuel, thereby protecting itself against rising fuel costs.

Equity Swap: In an equity swap, two parties agree to exchange cash flows based on the performance of an equity asset, such as a stock or an equity index, over a specified period. The cash flows exchanged typically involve one party paying a return based on the performance of the equity asset, while the other party pays a return based on another financial metric, such as a fixed interest rate, a floating interest rate, or the performance of another equity or asset class.

Credit Default Swaps (CDS): A credit default swap is a type of swap that acts like insurance against the default of a borrower. One party pays a periodic fee (premium) to another party, who agrees to compensate the first party if a specified credit event, like a default, occurs. An investor holding corporate bonds might buy a CDS to protect against the risk of the bond issuer defaulting on its debt.

Swaps are often used to hedge against risks such as interest rate fluctuations, currency exchange rate changes, or commodity price volatility. Traders may also use swaps to speculate on changes in market conditions without needing to own the underlying assets. Companies may use swaps to obtain more favorable loan terms or to manage cash flows in different currencies.

What’s the difference between linear and non-linear derivatives?

The difference between linear and non-linear derivatives primarily lies in how their value responds to changes in the underlying asset or reference rate.

Differentiation Factor | Linear Derivatives | Non-Linear Derivatives |

Payoff Structure | Proportional to the underlying asset's price movement. | Non-proportional, often complex and dependent on multiple factors. |

Financial Instruments | Futures, forwards, swaps | Options, structured products (options on swaps) |

Delta | Constant, typically 1 (or -1 for short positions), reflecting a direct one-to-one relationship with the underlying asset's price. | Variable, ranges between 0 to 1 (for calls) or 0 to -1 (for puts), and changes with the underlying asset’s price, time to expiration, and volatility. |

Sensitivity to Underlying Asset | Directly proportional; derivative price changes at a constant rate relative to the underlying asset. | Sensitivity varies; derivative price changes at a non-linear rate depending on factors like moneyness, time decay, and volatility. |

Risk Profile | Symmetric; risk and reward are directly correlated with the underlying asset’s price movement. | Asymmetric; risk and reward are influenced by the non-linear payoff structure, making the potential outcomes more complex. |

Behavior Near-Expiry | Consistent behavior throughout the life of the contract. | Delta and sensitivity can increase significantly near expiration, especially for at-the-money options. |

Complexity | Lower complexity, easier to manage and predict. | Higher complexity, requires advanced understanding and modeling. |

Valuation | Valuation is relatively straightforward and often based on the current price of the underlying asset and the contract terms. | Valuation is more complex, often requiring models like the Black-Scholes model (for options) that consider factors such as volatility, time to expiration, and the underlying asset's price. |

Linear derivatives are financial instruments whose value changes in direct proportion to changes in the price of the underlying asset. The payoff profiles of these derivatives are straightforward and typically follow a linear relationship with the underlying.

for examples,

Futures Contracts: The value of a futures contract moves in a linear fashion with the price of the underlying asset. For every $1 change in the underlying asset, the value of the futures contract also changes by $1.

Forwards: Similar to futures, the value of a forward contract changes linearly with the underlying asset's price.

Swaps: The cash flows in interest rate swaps, currency swaps, and similar contracts are usually linear, based on the difference between fixed and floating rates.

»» The payoff is directly proportional to the changes in the underlying asset. Valuation is generally simpler and more straightforward compared to non-linear derivatives. Gains and losses are symmetric, meaning they move equally in either direction based on the underlying asset's movement.

Non-linear derivatives are financial instruments whose value does not change proportionally with the price of the underlying asset. These derivatives have more complex payoff structures, often involving features like optionality, convexity, or leverage.

for examples,

Options (Calls and Puts): The value of an option is non-linear because the payoff depends on the underlying asset's price relative to the strike price. The relationship is influenced by factors like volatility, time decay, and the option's moneyness.

Convertible Bonds: These are bonds that can be converted into a predetermined number of shares of the issuing company. The non-linear aspect arises from the option to convert, which depends on the price of the stock.

Structured Products: These often combine linear instruments (like bonds) with non-linear components (like options), resulting in a non-linear payoff.

»» Non-linear derivatives often exhibit asymmetric payoffs. For example, an option holder can experience unlimited gains if the underlying asset moves favorably but has limited losses if it moves unfavorably. Valuing non-linear derivatives requires advanced mathematical models, often incorporating factors like volatility, time decay, and interest rates. Many non-linear derivatives exhibit convexity, where the sensitivity to changes in the underlying asset's price increases as the price moves in a certain direction (for example, gamma in options).

What are the differences between futures and forward derivatives?

Here are some differences between the two:

Meaning: forward contracts are agreements entered into by two parties (buyer and seller) to trade an asset at some future date at an agreed price/rate while futures contracts are agreements entered by a party (buyer or seller) with an Exchange with standardized terms.

Trading: forward contracts are traded over the counter (negotiated) between two parties while futures contracts are traded on the Exchange platform where one party is the buyer/seller and the other is the exchange.

Standardization: forward contracts are non-standardized contracts where the terms such as forward price/rate, lot size, maturity date, asset quality, etc. are agreed upon between both parties while futures contracts are highly standardized.

Settlement: forward contracts are settled on the maturity date, the date agreed upon by both parties in the contract, usually with physical delivery while future contracts are settled on a daily basis, and that too mark-to-market cash.

Margin/Collateral Requirements: theoretically, forward contracts have no requirement to post collateral at any point while futures contracts require a margin at initial, some maintenance margin, and a variation margin.

Regulation: theoretically, forward contracts are not regulated by any authority/exchange (self-regulated) while futures contracts are regulated by the exchange commission.

Credit Risk: forward contracts are exposed to counterparty risk as the other party may default on his obligations while futures contracts have almost zero counterparty risk as there is no possibility of default due to daily the mark-to-market feature.

Liquidity Risk: forward contracts are less liquid as a forward contract can only be terminated between the agreed parties while futures contracts can easily be liquidated on the exchange platform and hence involve less liquidity risk.

Best Use: forward contracts are recommended best for hedging financial risk as they are highly customizable while futures contracts are appropriate for speculation as they have almost zero counterparty risk with ease to exit from the contract.

What’s the difference between over-the-counter (OTC) and exchange-traded (ET) markets?

The difference between Over-the-Counter (OTC) and Exchange-Traded Markets primarily revolves around how financial instruments are traded, the level of regulation, and the risks involved.

Differentiation Factor | Over-the-Counter (OTC) Market | Exchange-Traded (ET) Market |

Definition | Decentralized market where trades are conducted directly between two parties, often via electronic networks or phone. Contracts are customized and negotiated privately. | Centralized market where standardized contracts are traded on organized exchanges like the NYSE, CME, or NSE, with all participants following the same rules. |

Counterparty Risk | Higher counterparty risk due to the absence of an intermediary guaranteeing the transaction. However, the use of Central Counterparties (CCPs) in some OTC markets has reduced this risk. | Lower counterparty risk because the exchange or a clearinghouse acts as an intermediary, ensuring that both sides of the transaction fulfill their obligations. |

Transparency | Limited transparency; prices and terms are privately negotiated, often leading to less visibility in the broader market. | High transparency; prices, volumes, and other market data are publicly available in real-time, allowing all participants to see the same information. |

Regulation | Less regulated; the level of regulation varies depending on the jurisdiction and the type of instrument. The use of CCPs in OTC markets has led to increased regulatory oversight. | Highly regulated by government agencies and market authorities, ensuring that the market operates fairly and participants are protected. |

Product Standardization | Contracts are highly customized to meet the specific needs of the parties involved, allowing for flexibility but making them less liquid. | Contracts are standardized in terms of size, expiration, and settlement terms, which enhances liquidity and ease of trading. |

Liquidity | Generally lower liquidity due to the customized nature of contracts, making it more difficult to find a counterparty. | Higher liquidity because of the standardized contracts and larger number of market participants, making it easier to enter and exit positions. |

Settlement Process | Settlement terms are negotiated between the parties and can vary widely. The introduction of CCPs has standardized some settlement processes in OTC markets. | Standardized settlement processes managed by the exchange or clearinghouse, typically involving daily mark-to-market and margin requirements. |

Cost | Potentially lower upfront costs due to direct negotiation, but can incur higher overall costs due to wider spreads and negotiation complexities. The use of CCPs may increase costs due to clearing fees. | Typically higher upfront costs due to exchange fees, but lower overall costs thanks to tighter spreads, lower risk, and reduced negotiation time. |

Flexibility | Offers greater flexibility in terms of contract customization, allowing parties to negotiate specific terms that fit their needs. | Less flexibility as all contracts are standardized, leaving no room for negotiation of terms. |

Market Participants | Generally used by institutional investors, corporations, and sophisticated investors due to the complexity and customization involved. The use of CCPs has made OTC markets more accessible. | Accessible to a broader range of participants, including retail investors, due to standardization, regulation, and ease of trading. |

»» Over-the-counter markets offer more customization and flexibility but come with higher counterparty risk, lower liquidity, and less regulation and transparency. Exchange-traded markets provide standardized contracts with greater liquidity, lower counterparty risk, and higher regulation and transparency.

Comments